Subscribe with RSS Reader

Subscribe with RSS ReaderOpen House today, 2:00PM - 4:00pm!

Open House today, 2:00PM - 4:00pm!

Posted on

April 20, 2025

by

Steve Flynn

Bank of Canada Interest Rate Announcement – April 16, 2025

Posted on

April 18, 2025

by

Steve Flynn

The Bank of Canada held its overnight policy rate at 2.75 per cent this morning. In the statement accompanying the decision, the Bank noted that pervasive uncertainty makes it unusually challenging to project GDP growth and inflation in Canada. The Bank sees two potential scenarios for the Canadian economy, either high but limited tariffs that temporarily weaken growth or a protracted trade war that causes both a full recession and inflation to rise above 3 per cent. The Bank is already seeing signs of a slower economy due to the impact of uncertainty on consumer and business confidence, but expects tariff driven supply chain disruptions will put upward pressure on prices later this year. Perhaps most importantly, the Bank ended its statement with the following: "Monetary policy cannot resolve trade uncertainty or offset the impacts of a trade war. What it can and must do is maintain price stability for Canadians." Copyright British Columbia Real Estate Association. Reprinted with permission. Open House. Open House on Sunday, April 20, 2025 2:00PM - 4:00PM

Posted on

April 18, 2025

by

Steve Flynn

Posted in

Sapperton, New Westminster Real Estate

Please visit our Open House at 204 258 Nelson's Court in New Westminster.

Open House on Sunday, April 20, 2025 2:00PM - 4:00PM MODERN & sleek, 876 s.f, 2 bed/2 bath condo in New West's dynamic Brewery District neighbourhood. OPEN & bright concept w/stylish kitchen, dining & living room. Kitchen has LUXURY features: s/s appliances, quartz countertops & gas stove. Both bedrooms are decent-sized. 2 balconies, totaling approx 200 s.f. Excellent building amenities incl: party room, outdoor kitchen/bbq & dining area, dog park & dog wash, community garden plots + access to amazing Club Central w/gym, squash, sauna, steam, social kitchen + games room. 2 PETS & RENTALS allowed! 1 parking, 1 locker. Within 5 min walk: Sapperton Skytrain, Royal Columbian Hospital, Save-On Foods, Shoppers, TD Bank & lots of restaurants. This is urban living at its best! OPEN HOUSE: Sun. Apr 20, 2-4pm! Canadian Inflation (March 2025) – April 15, 2025

Posted on

April 16, 2025

by

Steve Flynn

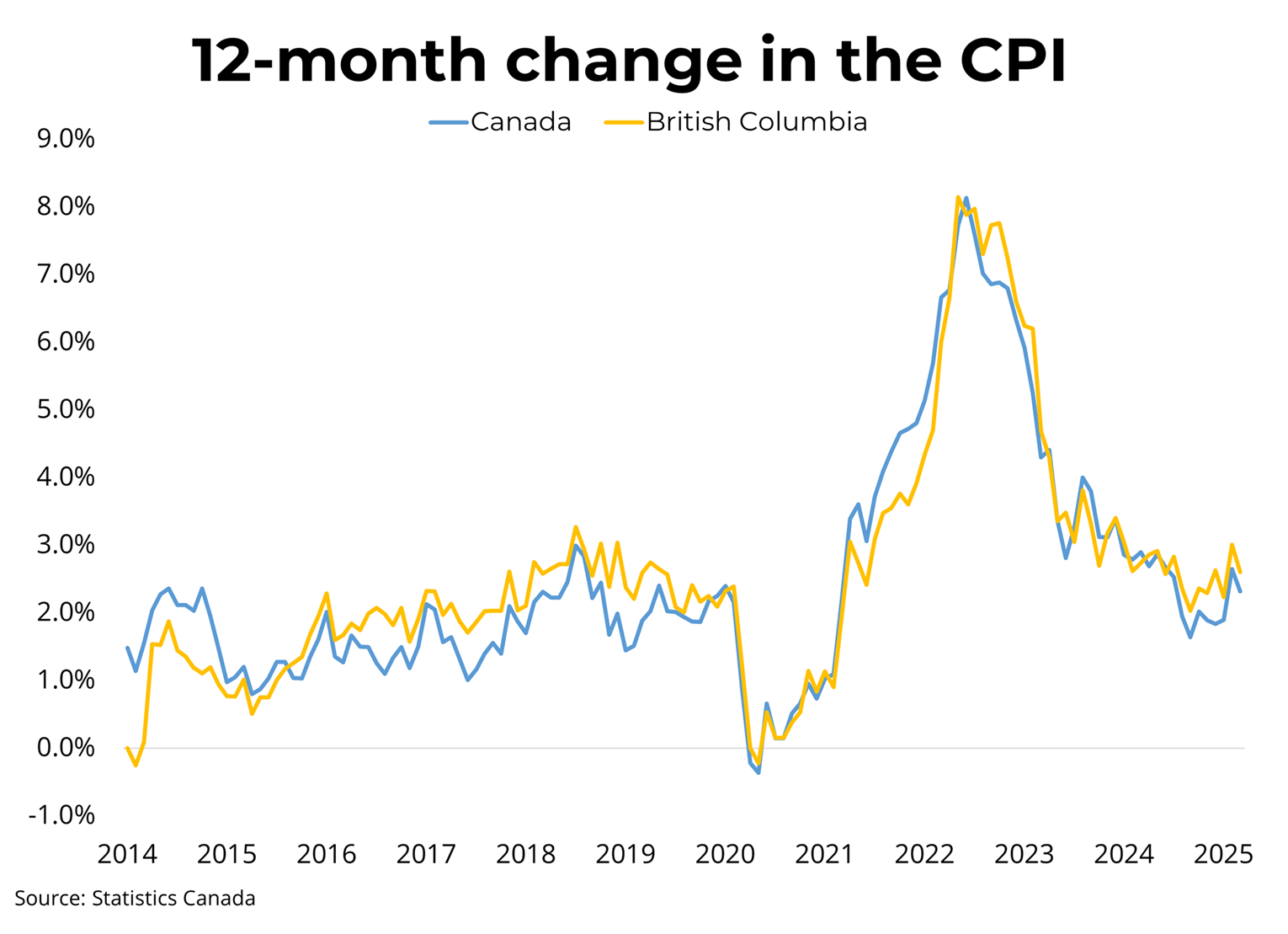

Canadian prices, as measured by the Consumer Price Index (CPI), rose 2.3 per cent on a year-over-year basis in March, down from a 2.6 per cent increase in February. Month-over-month, on a seasonally adjusted basis, the CPI was unchanged in March. The overall slowdown in headline CPI is largely driven by lower gasoline prices, with the CPI ex-gasoline rising by 2.5 per cent in March. Shelter price growth continues to cool, as mortgage interest costs were up 7.9 per cent, marking the nineteenth consecutive month of deceleration. Similarly, rent was up 5.1 per cent year-over-year in March, down from 5.8 per cent in February. In BC, consumer prices rose 2.6 per cent year-over-year, down from 3.0 per cent in February. The Bank of Canada's preferred measures of median and trimmed inflation, which strip out volatile components, are at 2.9 per cent and 2.8 per cent year-over-year, respectively. Copyright British Columbia Real Estate Association. Reprinted with permission. BC MLS Sales for March 2025

Posted on

April 15, 2025

by

Steve Flynn

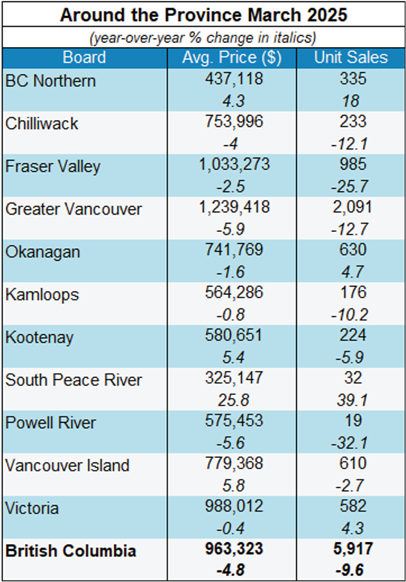

Vancouver, BC – April 14, 2025. The British Columbia Real Estate Association (BCREA) reports that 5,917 residential unit sales were recorded in Multiple Listing Service® (MLS®) Systems in March 2025, down 9.6 per cent from March 2024. The average MLS® residential price in BC in March 2025 was down 4.8 per cent at $963,323 compared to $1,011,965 in March 2024. The total sales dollar volume was $5.7 billion, a 13.9 per cent decrease from the same time the previous year. BC MLS® unit sales were 35 per cent lower than the ten-year March average. Open House today, 2:00PM - 4:00pm!

Posted on

April 13, 2025

by

Steve Flynn

New property listed in Sapperton, New Westminster

Posted on

April 10, 2025

by

Steve Flynn

Posted in

Sapperton, New Westminster Real Estate

I have listed a new property at 204 258 Nelson's Court in New Westminster.

MODERN & sleek, 876 s.f, 2 bed/2 bath condo in New West's dynamic Brewery District neighbourhood. OPEN & bright concept w/stylish kitchen, dining & living room. Kitchen has LUXURY features: s/s appliances, quartz countertops & gas stove. Both bedrooms are decent-sized. 2 balconies, totaling approx 200 s.f. Excellent building amenities incl: party room, outdoor kitchen/bbq & dining area, dog park & dog wash, community garden plots + access to amazing Club Central w/gym, squash, sauna, steam, social kitchen + games room. 2 PETS & RENTALS allowed! 1 parking, 1 locker. Within 5 min walk: Sapperton Skytrain, Royal Columbian Hospital, Save-On Foods, Shoppers, TD Bank & lots of restaurants. This is urban living at its best! OPEN HOUSE: Sun. Apr 13, 2-4pm. Open House. Open House on Sunday, April 13, 2025 2:00PM - 4:00PM

Posted on

April 10, 2025

by

Steve Flynn

Posted in

Sapperton, New Westminster Real Estate

Please visit our Open House at 204 258 Nelson's Court in New Westminster.

Open House on Sunday, April 13, 2025 2:00PM - 4:00PM MODERN & sleek, 876 s.f, 2 bed/2 bath condo in New West's dynamic Brewery District neighbourhood. OPEN & bright concept w/stylish kitchen, dining & living room. Kitchen has LUXURY features: s/s appliances, quartz countertops & gas stove. Both bedrooms are decent-sized. 2 balconies, totaling approx 200 s.f. Excellent building amenities incl: party room, outdoor kitchen/bbq & dining area, dog park & dog wash, community garden plots + access to amazing Club Central w/gym, squash, sauna, steam, social kitchen + games room. 2 PETS & RENTALS allowed! 1 parking, 1 locker. Within 5 min walk: Sapperton Skytrain, Royal Columbian Hospital, Save-On Foods, Shoppers, TD Bank & lots of restaurants. This is urban living at its best! OPEN HOUSE: Sun. Apr 13, 2-4pm. Open House today at 204-258 NELSON'S Court in New Westminster, 2:00PM - 4:00pm!

Posted on

April 6, 2025

by

Steve Flynn

Listed at $749,000 MODERN & sleek, 876 s.f, 2 bed/2 bath condo in New West's dynamic Brewery District neighbourhood. OPEN & bright concept w/stylish kitchen, dining & living room. Kitchen has LUXURY features: s/s appliances, quartz countertops & gas stove. Both bedrooms are decent-sized. 2 balconies, totaling approx 200 s.f. Excellent building amenities incl: party room, outdoor kitchen/bbq & dining area, dog park & dog wash, community garden plots + access to amazing Club Central w/gym, squash, sauna, steam, social kitchen + games room. 2 PETS & RENTALS allowed! 1 parking, 1 locker. Within 5 min walk: Sapperton Skytrain, Royal Columbian Hospital, Save-On Foods, Shoppers, TD Bank & lots of restaurants. This is urban living at its best! Canadian Employment (March 2025) – April 4, 2025

Posted on

April 5, 2025

by

Steve Flynn

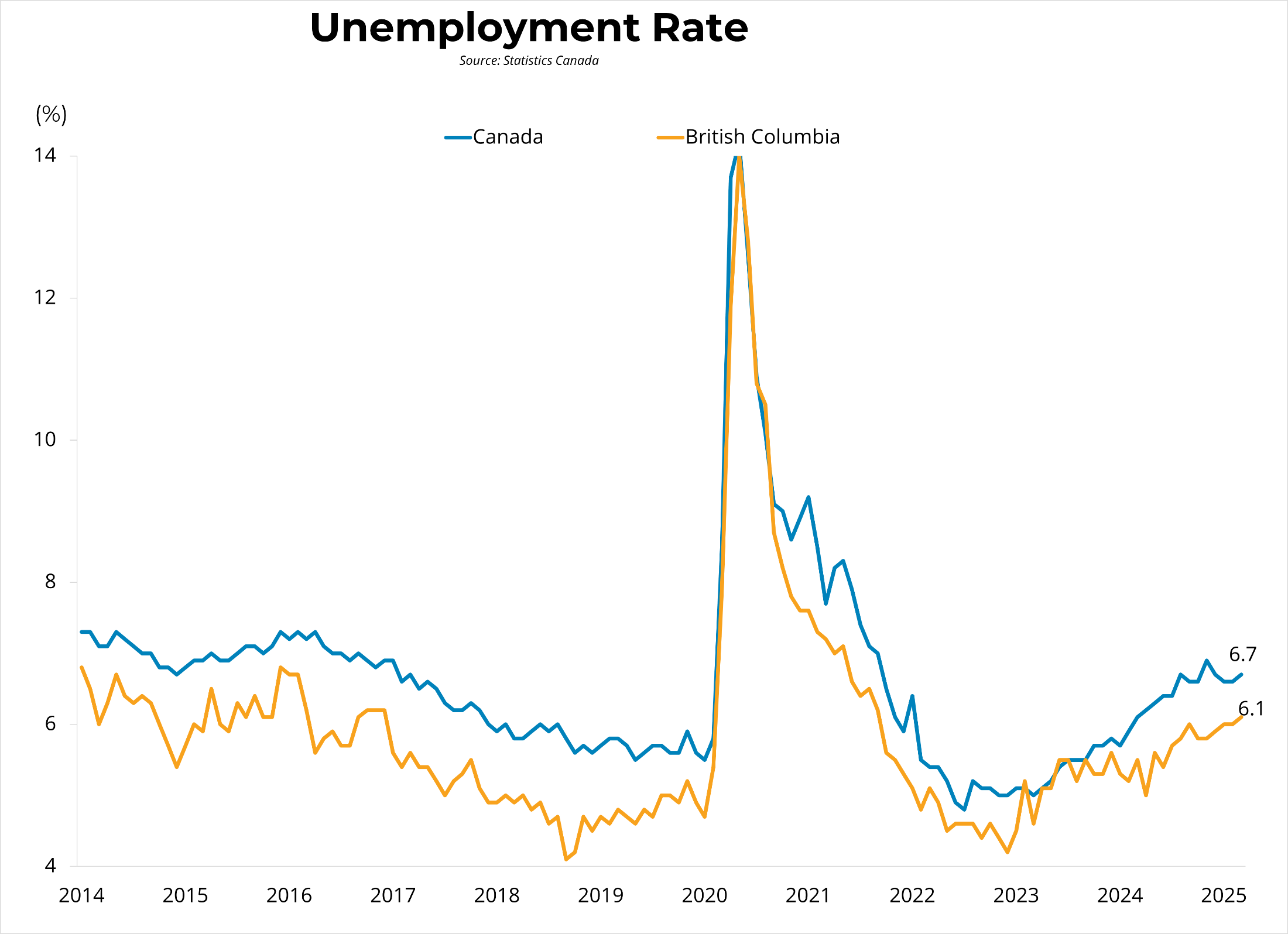

Canadian employment fell by 0.2 per cent from the previous month, declining by 33,000 jobs to 20.962 million in March. The employment rate fell by 0.2 points to 60.9 per cent, while the unemployment rate rose by 0.1 points to 6.7 per cent. Average hourly wages rose 3.6 per cent year-over-year to $36.05 last month, while total hours worked were up 1.2 per cent compared to March of the previous year. Copyright British Columbia Real Estate Association. Reprinted with permission. New property listed in Bolivar Heights, North Surrey

Posted on

April 5, 2025

by

Steve Flynn

I have listed a new property at 14073 113 Avenue in Surrey.

OPPORTUNITY awaits for builders or investors. 8345 sq ft lot with R3 zoning. 4 bed, 2.5 bath, 2730 sq ft bungalow w/legal 2 bed, 1 bath suite below on quiet, dead-end street. Transit, Surrey Traditional School & James Ardiel Elementary school only 1-3 blocks away! Separate garage, parking for 6 vehicles on property. Large north-facing yard. Close to Guildford Mall, Central City, King George Boulevard, Hwy 17 & Hwy 1. House in original condition. Quick Snapshot of METRO VANCOUVER'S March 2025 MLS Sales

Posted on

April 4, 2025

by

Steve Flynn

The MLS® Home Price Index composite benchmark price for all residential properties in Metro Vancouver* is $1,190,900. This represents a 0.6 per cent decrease over March 2024 and a 0.5 per cent increase compared to February 2025. Specifically: - The benchmark price for detached homes increased 0.8% from Mar 2024 and increased 0.4% from Feb 2025. - The benchmark price for townhouses/attached decreased 0.8% from Mar 2024 and increased 0.2% from Feb 2025. - The benchmark price for apartment/condos decreased 0.9% from Mar 2024 and increased 1.0% from Feb 2025. *Areas covered by the Real Estate Board of Greater Vancouver include: Burnaby, Coquitlam, Maple Ridge, New Westminster, North Vancouver, Pitt Meadows, Port Coquitlam, Port Moody, Richmond, South Delta, Squamish, Sunshine Coast, Vancouver, West Vancouver, and Whistler. JUST LISTED!

Posted on

April 4, 2025

by

Steve Flynn

Metro Vancouver March 2025 MLS Sales

Posted on

April 3, 2025

by

Steve Flynn

Home sales registered on the MLS® in Metro Vancouver* for the month of March were the lowest going back to 2019 for the same month, while active listings continue to their upward trend. The Greater Vancouver REALTORS® (GVR) reports that residential sales in the region totalled 2,091 in March 2025, a 13.4 per cent decrease from the 2,415 sales recorded in March 2024. This was 36.8 per cent below the 10-year seasonal average (3,308). “If we can set aside the political and economic uncertainty tied to the new U.S. administration for a moment, buyers in Metro Vancouver haven’t seen market conditions this favourable in years,” said Andrew Lis, GVR’s director of economics and data analytics. “Prices have eased from recent highs, mortgage rates are among the lowest we’ve seen in years, and there are more active listings on the MLS® than we’ve seen in almost a decade. Sellers appear ready to engage — but so far, buyers have not shown up in the numbers we typically see at this time of year.” There were 6,455 detached, attached and apartment properties newly listed for sale on the Multiple Listing Service® (MLS®) in Metro Vancouver in March 2025. This represents a 29 per cent increase compared to the 5,002 properties listed in March 2024. This was 15.8 per cent above the 10-year seasonal average (5,572). The total number of properties currently listed for sale on the MLS® system in Metro Vancouver is 14,546, a 37.9 per cent increase compared to March 2024 (10,552). This is 44.9 per cent above the 10-year seasonal average (10,038). Across all detached, attached and apartment property types, the sales-to-active listings ratio for March 2025 is 14.9 per cent. By property type, the ratio is 10.3 per cent for detached homes, 21.5 per cent for attached, and 16.2 per cent for apartments. Analysis of the historical data suggests downward pressure on home prices occurs when the ratio dips below 12 per cent for a sustained period, while home prices often experience upward pressure when it surpasses 20 per cent over several months. “The current market bares resemblance to early 2023 where price trends were generally flat, and sales started the year off slowly before gaining momentum in the spring and summer months,” Lis said. “While market conditions overall remain balanced, it’s worth noting that the attached segment continues teetering on the threshold of a sellers’ market as a result of a chronic undersupply, with only about 2,200 active listings available for prospective buyers throughout the entire region.” The MLS® Home Price Index composite benchmark price for all residential properties in Metro Vancouver is currently $1,190,900. This represents a 0.6 per cent decrease over March 2024 and a 0.5 per cent increase compared to February 2025. Sales of detached homes in March 2025 reached 527, a 24.1 per cent decrease from the 694 detached sales recorded in March 2024. The benchmark price for a detached home is $2,034,400. This represents a 0.8 per cent increase from March 2024 and a 0.4 per cent increase compared to February 2025. Sales of apartment homes reached 1,084 in March 2025, a 10.2 per cent decrease compared to the 1,207 sales in March 2024. The benchmark price of an apartment home is $767,300. This represents a 0.9 per cent decrease from March 2024 and a 1 per cent increase compared to February 2025. Attached home sales in March 2025 totalled 472, a 4.6 per cent decrease compared to the 495 sales in March 2024. The benchmark price of a townhouse is $1,113,100. This represents a 0.8 per cent decrease from March 2024 and a 0.2 per cent increase compared to February 2025. *Areas covered by the Real Estate Board of Greater Vancouver include: Burnaby, Coquitlam, Maple Ridge, New Westminster, North Vancouver, Pitt Meadows, Port Coquitlam, Port Moody, Richmond, South Delta, Squamish, Sunshine Coast, Vancouver, West Vancouver, and Whistler. Canadian Economic Growth (January 2025) – March 29, 2025

Posted on

March 30, 2025

by

Steve Flynn

Canadian real GDP increased by 0.4 per cent in January, following a 0.3 per cent increase in December. Service-producing industries grew by 0.1 per cent, while goods-producing industries rose by 1.1 per cent. Thirteen out of twenty major industries expanded from the previous month, led by mining, quarrying, and oil/gas extraction (1.7 per cent), construction (0.7 per cent), and manufacturing (0.8 per cent). Finally, GDP for real-estate offices and agents was down 3.7 per cent month-over-month. Preliminary estimates suggest that real GDP was unchanged in February. Copyright British Columbia Real Estate Association. Reprinted with permission. Canadian Retail Sales (January 2025) – March 22, 2025

Posted on

March 23, 2025

by

Steve Flynn

Canadian retail sales decreased by 0.6 per cent to $69.4 billion in January from the previous month. Compared to the same time last year, retail sales are up by 4.2 per cent. Furthermore, core retail sales, which exclude gasoline and automobile items, fell by 0.2 per cent month-over-month. In volume terms, adjusted for rising prices, retail sales decreased by 1.1 per cent in January. Copyright British Columbia Real Estate Association. Reprinted with permission. Canadian Inflation (February 2025) – March 18, 2025

Posted on

March 19, 2025

by

Steve Flynn

Canadian prices, as measured by the Consumer Price Index (CPI), rose 2.6 per cent on a year-over-year basis in February, up from a 1.9 per cent increase in January. Month-over-month, on a seasonally adjusted basis, CPI increased by 0.7 points in February. Products affected by the end of the GST/HST tax break saw slower year-over-year price declines compared to previous months, placing upward pressure on headline inflation. Overall, shelter price growth continues to cool, as mortgage interest costs were up 9.0 per cent, marking the eighteenth consecutive month of deceleration. Similarly, rent was up 5.8 per cent in February year-over-year, down from 6.3 per cent in January. In BC, consumer prices rose 3.0 per cent year-over-year, up from 2.2 per cent in January. The Bank of Canada's preferred measures of median and trimmed inflation, which strip out volatile components, both rose to 2.9 per cent year-over-year. Copyright British Columbia Real Estate Association. Reprinted with permission. Canadian Housing Starts (February 2025) – March 17, 2025

Posted on

March 18, 2025

by

Steve Flynn

Canadian housing starts fell by 4 per cent to 229,030 units in February at a seasonally adjusted annual rate (SAAR). Starts were down 12 per cent from the same month last year. Single-detached housing starts fell by 1 per cent from last month to 56,273 units, while multi-family and other starts dropped by 5 per cent to 172,759 units (SAAR). Copyright British Columbia Real Estate Association. Reprinted with permission. I have sold a property at 101 9300 UNIVERSITY CRES in Burnaby

Posted on

March 18, 2025

by

Steve Flynn

I have sold a property at 101 9300 UNIVERSITY CRES in Burnaby.

STYLISH & modern, 975 sq ft, 2 bed/2 bath ground floor condo in One University Crescent at SFU. On north-west corner w/lots of windows & breezes. Recently updated w/new flooring, paint, lighting, window coverings, storage, hardware & fixtures throughout + amazing high-end kitchen w/marble finishes, coffee station & Fischer Paykel appliances! The 2 bedrooms are very good-sized & located for ideal privacy. Approx 220 sq ft private deck, perfect for gardeners. Building amenities incl: party room, billiards room, gym & ev-charging in parkade. 1 parking, 1 locker. 1 pet & rentals allowed. Prepaid SFU lease, expires 2102. Surrounded by trails & nature yet SFU, University Highands Elementary, Nester's Market, Scotiabank & many services & dining are within 3 blocks. Just SOLD: 101-9300 UNIVERSITY Crescent, Burnaby

Posted on

March 16, 2025

by

Steve Flynn

STYLISH & modern, 975 sq ft, 2 bed/2 bath ground floor condo in One University Crescent at SFU. On north-west corner w/lots of windows & breezes. Recently updated w/new flooring, paint, lighting, window coverings, storage, hardware & fixtures throughout + amazing high-end kitchen w/marble finishes, coffee station & Fischer Paykel appliances! The 2 bedrooms are very good-sized & located for ideal privacy. Approx 220 sq ft private deck, perfect for gardeners. Building amenities incl: party room, billiards room, gym & ev-charging in parkade. 1 parking, 1 locker. 1 pet & rentals allowed. Prepaid SFU lease, expires 2102. Surrounded by trails & nature yet SFU, University Highands Elementary, Nester's Market, Scotiabank & many services & dining are within 3 blocks.

Categories:

Abbotsford West, Abbotsford Real Estate

|

Bolivar Heights, North Surrey Real Estate

|

Brentwood Park, Burnaby North Real Estate

|

Brighouse, Richmond Real Estate

|

Burnaby

|

Burnaby Real Estate

|

Burnaby South Real Estate

|

Cape Horn, Coquitlam Real Estate

|

Cariboo, Burnaby North Real Estate

|

Central BN, Burnaby North Real Estate

|

Central Coquitlam, Coquitlam

|

Central Coquitlam, Coquitlam Real Estate

|

Champlain Heights, Vancouver East

|

Champlain Heights, Vancouver East Real Estate

|

Cloverdale BC, Cloverdale Real Estate

|

Cloverdale BC, Surrey Real Estate

|

Cloverdale Real Estate

|

Coal Harbour, Vancouver West Real Estate

|

Coaquitlam

|

College Park PM, Port Moody Real Estate

|

Collingwood VE, Vancouver East Real Estate

|

Coquitlam

|

Coquitlam West, Coquitlam Real Estate

|

Downtown NW, New Westminster Real Estate

|

Downtown VW, Vancouver West

|

Downtown VW, Vancouver West Real Estate

|

Eagleridge, Coquitlam Real Estate

|

False Creek North, Vancouver West

|

Fraserview NW, New Westminster

|

Fraserview NW, New Westminster Real Estate

|

Fraserview VE, Vancouver East Real Estate

|

GlenBrooke North, New Westminster Real Estate

|

Grandview Surrey, Surrey Real Estate

|

Harrison Hot Springs Real Estate

|

Hastings, Vancouver East Real Estate

|

Highgate, Burnaby South Real Estate

|

Hockaday, Coquitlam Real Estate

|

January 2014 Sales in Greater Vancouver

|

Metrotown, Burnaby South Real Estate

|

New Horizons, Coquitlam Real Estate

|

New Westminster Real Estate

|

Port Moody

|

Port Moody Real Estate

|

Quay, New Westminster Real Estate

|

Queensborough, New Westminster Real Estate

|

Richmond Real Estate

|

Riverdale RI, Richmond Real Estate

|

Riverwood, Port Coquitlam Real Estate

|

Sapperton, New Westminster Real Estate

|

Simon Fraser Univer., Burnaby North Real Estate

|

Surrey

|

The Heights NW, New Westminster

|

The Heights NW, New Westminster Real Estate

|

Tsawwassen Central, Tsawwassen Real Estate

|

Uptown NW, New Westminster Real Estate

|

Uptown, New Westminster Real Estate

|

Vancouver

|

Vancouver East Real Estate

|

Videocast of January 2014 sales

|

Walnut Grove, Langley Real Estate

|

West Central, Maple Ridge Real Estate

|

West End VW, Vancouver West Real Estate

|

Whalley, North Surrey Real Estate

|

Whalley, Surrey Real Estate

|

Willoughby Heights, Langley Real Estate

|

Let's discuss your next home sale or purchase, with no obligation.

Give me a call at 604.785.3977

Crest Realty - Burnaby

Crest Realty - Burnaby